If there is one investment approach that has stood the test of time, been endorsed by the world’s greatest investors including Warren Buffett, and consistently outperformed the majority of professional fund managers — it is investing in index funds.

Index funds are not glamorous. They do not promise to double your money in a year. They will not give you a hot tip or an exciting story to tell at dinner parties. But for long-term wealth building, very few investment vehicles come close to their combination of simplicity, low cost, and consistent performance.

This guide explains what index funds are, how to evaluate them, and how to use them to build lasting wealth.

What Is an Index Fund?

An index fund is a type of investment fund — either a mutual fund or an ETF (Exchange Traded Fund) — that tracks a specific market index. Rather than having a fund manager actively pick stocks, the fund simply buys all (or a representative sample) of the stocks in the index it tracks.

For example:

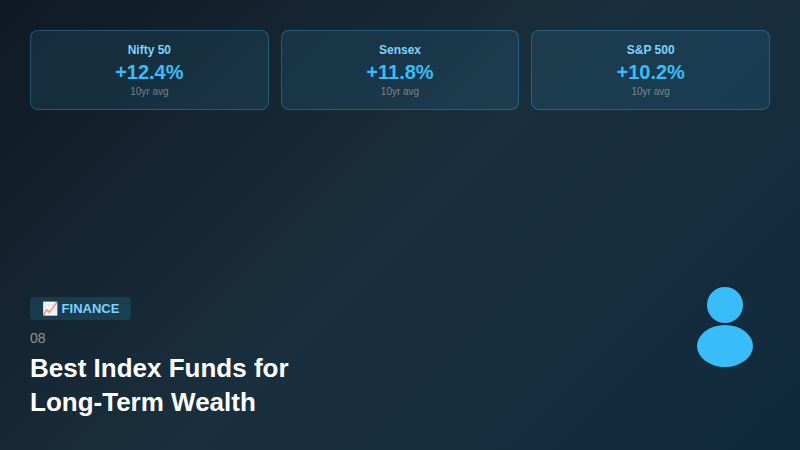

- A fund tracking the S&P 500 holds shares in the 500 largest US companies

- A fund tracking the NIFTY 50 holds shares in the 50 largest Indian companies by market capitalization

- A global index fund might track thousands of companies across multiple countries

Because there is no active management — no team of analysts researching stocks and making buy/sell decisions — the costs of running an index fund are much lower than actively managed funds.

Why Index Funds Beat Most Active Fund Managers

This might sound surprising, but decades of research and real-world data consistently show that the majority of professionally managed, actively trading funds underperform simple index funds over the long term.

The reasons are straightforward:

Higher costs eat into returns. Active funds charge significantly higher management fees (expense ratios). Over 20–30 years, even a seemingly small difference in fees compounds into a massive difference in final wealth.

Beating the market is genuinely hard. Markets are highly efficient — millions of smart, well-resourced investors are all trying to find undervalued stocks at the same time. Consistently finding stocks that others have missed is extremely difficult, even for professionals.

Tax efficiency. Index funds buy and sell stocks far less frequently than active funds. This generates fewer taxable events, which improves net returns for investors.

Warren Buffett himself has said that for most investors, putting money in a low-cost S&P 500 index fund and holding it long-term will beat the vast majority of investment professionals over time.

Key Factors to Evaluate When Choosing an Index Fund

1. Expense Ratio

The expense ratio is the annual fee charged by the fund, expressed as a percentage of your investment. For index funds, look for expense ratios as low as possible — ideally below 0.20% for broad market funds. Many of the best index funds charge between 0.03% and 0.10%.

Over 30 years, the difference between a 0.05% and a 1.5% expense ratio on the same investment can result in tens of thousands of additional dollars in your pocket.

2. Index Being Tracked

Different indices have different characteristics. Broad market indices (tracking hundreds or thousands of companies) offer the most diversification. Sector-specific or thematic indices carry more concentration risk.

3. Tracking Error

This measures how closely the fund’s performance matches the index it tracks. A lower tracking error means the fund is doing its job more accurately. Look for funds with consistently low tracking error.

4. Fund Size and Liquidity

Larger, more established funds are generally more liquid, have tighter bid-ask spreads (for ETFs), and are less likely to close unexpectedly.

5. Fund House Reputation

Choose funds from established, reputable asset management companies with a long track record of managing index products.

Types of Index Funds for Long-Term Wealth Building

Broad Market Domestic Index Funds

Track the entire stock market of your country or a large representative portion of it. These are the core of most long-term portfolios. Examples include funds tracking the total market, the large-cap index, or the top companies by market capitalization in your country.

Best for: Core long-term holding, maximum diversification within one country

International / Global Index Funds

Track stock markets in other countries or globally. Adding international index funds to your portfolio reduces dependence on any single country’s economy.

Best for: Geographic diversification, exposure to global growth

Bond Index Funds

Track indices of government or corporate bonds rather than stocks. Lower returns than equity index funds, but much lower volatility. Useful for balancing a portfolio as you approach a financial goal.

Best for: Reducing portfolio volatility, medium-term goals, conservative investors

Small-Cap and Mid-Cap Index Funds

Track smaller companies rather than large blue chips. Historically, small-cap stocks have delivered higher long-term returns than large caps, but with greater short-term volatility.

Best for: Long-term investors seeking higher growth potential who can tolerate more volatility

A Simple Long-Term Portfolio Using Index Funds

For most investors building long-term wealth, a simple three-fund portfolio covers the essentials:

- Broad domestic market index fund — core holding, majority of portfolio

- International index fund — global diversification

- Bond index fund — stability and risk management (increase allocation as you get older)

The exact allocation depends on your age, risk tolerance, and time horizon. Younger investors typically hold more in equity index funds and less in bond funds. As retirement approaches, the allocation gradually shifts toward more bonds.

Rebalancing: The One Annual Task

Over time, the different parts of your portfolio will grow at different rates, causing your original allocation to drift. Once a year, review your portfolio and rebalance — selling a portion of the funds that have grown above their target allocation and buying more of those below target.

This annual discipline keeps your risk level consistent and actually improves returns over time by systematically buying low and selling high.

The Most Important Ingredient: Time

Index funds work best over long time horizons. The stock market experiences corrections, recessions, and crashes periodically — but historically, patient investors who stay invested through these periods are always rewarded eventually.

The key behaviors for index fund success are:

- Start as early as possible

- Invest consistently, especially during market downturns

- Minimize fees by choosing low-cost funds

- Never panic-sell during corrections

- Rebalance once a year and otherwise leave your portfolio alone

Final Thoughts

Index funds are one of the most powerful wealth-building tools available to ordinary investors. They require no special knowledge, no ongoing research, and very little time. They offer broad diversification, low costs, and historically strong long-term returns.

The best index fund is often the simplest, lowest-cost one that tracks a broad market index. Start early, invest consistently, keep costs low, and let compounding do the work over decades.