University is often the first time in your life that you are fully responsible for your own finances. Suddenly you are managing rent, groceries, course materials, transport, social activities, and unexpected expenses — all on a limited budget.

For most students, no one formally teaches them how to do this. And the consequences of poor money management during university years can follow you well beyond graduation — in the form of debt, stress, and missed opportunities to build an early financial foundation.

This complete guide covers everything a university student needs to know about managing money well, staying out of financial trouble, and actually coming out of university in a stronger financial position than when you started.

Why Money Management Matters in University

Poor money management during university is extremely common and has real consequences:

- Running out of money before the month ends

- Taking on unnecessary high-interest debt

- Missing academic opportunities due to financial stress

- Starting adult life with debt that takes years to repay

- Missing the early years of compounding by not starting to save and invest

Good money management during university, on the other hand, builds habits that will benefit you for the rest of your life — and can even allow you to graduate with some savings or investments already working for you.

Step 1: Know Your Total Monthly Income

Before you can manage your money, you need to know exactly how much you have coming in each month. Add up all sources:

- Parental allowance or family support

- Scholarship or bursary payments

- Part-time job income

- Student loan disbursements (treat these as money to be managed carefully, not a windfall)

- Any freelance or side income

Write this number down. This is your total monthly budget ceiling — you cannot spend more than this without going into debt.

Step 2: List All Fixed Monthly Expenses

Fixed expenses are costs that are the same every month regardless of what you do:

- Rent or accommodation fees

- Utility bills (if not included in rent)

- Mobile phone plan

- Transport pass or fuel costs

- Essential subscriptions (internet, cloud storage for coursework)

- Loan repayments (if any)

Subtract these from your monthly income. What remains is your discretionary budget — the money available for food, social activities, clothing, entertainment, and everything else.

Step 3: Budget for Variable Expenses

Variable expenses change month to month and are where most students lose control of their finances. Key categories:

Food and groceries — Set a weekly food budget and stick to it. Cooking your own meals instead of eating out or ordering delivery is one of the biggest money-savers available to students.

Social activities — It is important to have a social life, but it is also easy to overspend here. Set a monthly social budget and plan accordingly.

Books and course materials — Buy second-hand books where possible, use the library, and share course materials with classmates.

Clothing and personal items — Budget a small monthly allowance and avoid impulse purchases.

Entertainment — Streaming services, events, and hobbies. Keep this category honest and limited.

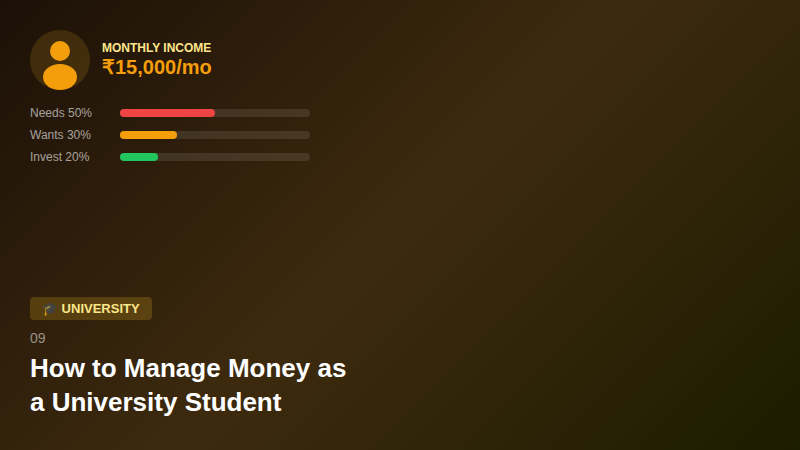

Step 4: The 50/30/20 Rule for Students

A simple framework that works well for students is the 50/30/20 rule:

- 50% of income → Needs (rent, food, transport, course materials)

- 30% of income → Wants (social activities, entertainment, non-essential spending)

- 20% of income → Saving and investing (emergency fund, investment account)

Even if you cannot hit exactly these percentages right away, using this framework as a target significantly improves your financial management.

Step 5: Build an Emergency Fund

An emergency fund is a small savings buffer — ideally one to two months of your essential expenses — kept in a separate account that you only touch in genuine emergencies.

This is your financial safety net. It prevents you from going into credit card debt or calling parents in a panic when unexpected expenses hit — a broken laptop, a medical bill, a sudden travel expense.

Build this before anything else. Once it is established, leave it alone.

Step 6: Avoid These Common Student Money Traps

Credit cards without discipline — A credit card used irresponsibly creates high-interest debt that grows rapidly. If you use a credit card, pay the full balance every month without exception.

Buy-now-pay-later schemes — These make purchases feel free in the short term but create debt obligations that pile up. Avoid them for non-essential purchases.

Student overdrafts misused — Many universities offer interest-free student overdrafts. These are a genuine safety net for genuine emergencies, not an extension of your budget for luxuries.

Lifestyle inflation — When a student loan comes in or you start earning from a part-time job, it is tempting to immediately increase spending. Resist this. Lifestyle inflation is how people perpetually feel broke regardless of how much they earn.

Ignoring student discounts — As a student you have access to significant discounts on transport, software, entertainment, food, and many services. Always ask if a student discount is available. These discounts can save a meaningful amount over the course of your degree.

Step 7: Earn More — Part-Time and Side Income

The most direct way to improve your financial situation as a student is to earn more. Options include:

Part-time employment — Campus jobs, retail, hospitality, tutoring, administrative work. Balance carefully with your academic workload.

Freelancing — If you have marketable skills (writing, design, coding, social media management, translation), freelance platforms allow you to earn on your own schedule.

Tutoring — If you perform well academically, tutoring younger students or peers in subjects you excel at is both profitable and flexible.

Selling unwanted items — Regular decluttering and selling unused items online generates occasional income and reduces clutter.

Any additional income should be directed primarily toward your emergency fund and savings goal before increasing spending.

Step 8: Start Saving and Investing Early

Once your emergency fund is built, start investing — even a small amount. Open a low-cost investment account and set up a monthly automatic investment into a diversified index fund or mutual fund SIP.

The purpose is not to get rich quickly during university. The purpose is to:

- Build the habit of investing consistently

- Give your money the maximum possible time to compound

- Graduate with an investment account that has already started growing

Step 9: Track Your Progress Monthly

At the end of each month, spend 15 minutes reviewing:

- Did you stay within your budget?

- Did you save your target amount?

- Were there unexpected expenses? How will you handle them next month?

- Did any expense category consistently go over budget?

Monthly reviews keep you honest, help you identify patterns, and allow you to adjust your budget as your situation changes.

Final Thoughts

Managing money well as a university student is not about depriving yourself of a good student experience. It is about making conscious choices with your money so that those choices serve you now and in the future.

Students who graduate with good financial habits, no consumer debt, and a small investment account already started are years ahead of their peers. The effort required is not enormous — it is mostly a matter of awareness, discipline, and a few good habits applied consistently.

Start now. Your future self will be grateful.