One of the most powerful yet underutilized wealth-building tools available to everyday investors is the Systematic Investment Plan, commonly known as SIP. It is not a specific type of fund — it is a method of investing. And it is a method that has helped millions of ordinary people across the world build significant wealth over time, without needing to be financial experts or having large sums of money to start.

This guide will explain exactly what SIP is, how it works, why it is so effective, and how you can use it to grow your money month by month starting today.

What Is a SIP?

A Systematic Investment Plan (SIP) is a way of investing a fixed amount of money at regular intervals — usually monthly — into a mutual fund of your choice.

Instead of investing a large lump sum all at once, you invest smaller amounts consistently over a long period. Each month, on a date you choose, a fixed amount is automatically deducted from your bank account and invested into your selected fund. You receive units of that fund at whatever the price is on that day.

That is the entire concept. Simple, but extraordinarily powerful.

How Does SIP Work in Practice?

Let us say you decide to invest a fixed amount every month into an equity mutual fund. Here is what happens:

- Month 1: Market is at a normal level. You invest your fixed amount and receive a certain number of units.

- Month 3: Market drops significantly. Your fixed amount now buys more units because the price per unit is lower.

- Month 7: Market recovers and rises. Your fixed amount buys fewer units, but the units you bought at lower prices are now worth more.

Over time, this process — called rupee-cost averaging or dollar-cost averaging — means your average cost per unit is lower than the average market price. You automatically buy more when markets are cheap and less when they are expensive, without having to time anything.

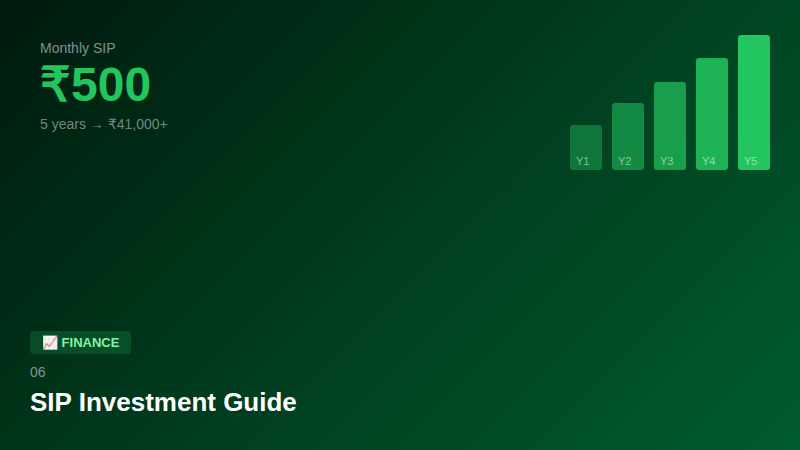

The Power of Compounding Through SIP

The real magic of SIP comes from the combination of consistent investing and compounding.

Compounding means your returns generate their own returns. In a SIP, every month you invest adds to a growing base, and all of it earns returns together. Over long periods, this creates exponential growth.

Here is an illustration of how monthly SIP investments grow over time at a hypothetical average annual return:

- After 5 years: Your total invested amount plus compounded growth is noticeably larger than what you put in

- After 10 years: The growth significantly accelerates — the gap between what you invested and what your portfolio is worth widens considerably

- After 20–30 years: The compounding effect becomes dramatic — the majority of your wealth is not from what you contributed, but from the returns earned on your returns

This is why starting a SIP early — even with a very small amount — is so much more valuable than starting later with a larger amount.

Key Benefits of SIP

1. No need to time the market One of the biggest mistakes investors make is trying to wait for the “perfect” time to invest. SIP removes this problem entirely. You invest every month regardless of market conditions. Over time, this averages out your purchase price and reduces the impact of market volatility.

2. Builds financial discipline Because SIP is automated, you invest consistently without having to remember to do it or make a decision each month. This builds the habit of investing and prevents the temptation to spend money that should be invested.

3. Starts with small amounts Many mutual fund platforms allow SIPs with very low minimum monthly amounts. This means anyone — students, young professionals, part-time workers — can start building wealth through SIP.

4. Flexibility You can increase your SIP amount when your income grows. Many investors use a “step-up SIP” where they increase their monthly contribution by a fixed percentage every year, significantly accelerating wealth accumulation over time.

You can also pause or stop a SIP if needed, and restart it later. This flexibility makes it suitable for investors at all income levels.

5. Professionally managed When you invest in a mutual fund via SIP, your money is managed by professional fund managers who research markets, analyze companies, and make investment decisions on your behalf.

Types of Mutual Funds for SIP

Equity funds — Invest primarily in stocks. Higher risk, higher potential returns. Best suited for long-term goals (5+ years).

Debt funds — Invest in bonds and fixed income instruments. Lower risk, more stable returns. Suitable for medium-term goals.

Hybrid funds — Invest in both stocks and bonds. A balanced approach for moderate risk tolerance.

Index funds — Track a market index passively. Very low management fees, consistent with market returns. Excellent choice for beginners.

For beginners, starting with a broad market index fund via SIP is often the simplest and most effective approach.

How to Start a SIP: Step-by-Step

Step 1: Complete KYC (Know Your Customer) verification on a mutual fund platform or through a registered financial intermediary.

Step 2: Choose the mutual fund that suits your goals and risk tolerance. For most beginners, a diversified equity index fund is a strong starting point.

Step 3: Decide your monthly SIP amount. Start with whatever you can comfortably commit to every month. You can always increase it later.

Step 4: Set your SIP date — typically aligned with your salary or income date, so funds are available.

Step 5: Automate — link your bank account and let the SIP run automatically every month.

Step 6: Review annually — check whether your fund is performing in line with its benchmark, and consider increasing your SIP amount each year.

Common SIP Mistakes to Avoid

Stopping SIP during market downturns — This is the worst thing you can do. Market dips are actually when SIP works best, buying more units at lower prices. Stay invested.

Choosing funds based on recent performance — Past performance does not guarantee future results. Choose funds based on long-term consistency, fund house reputation, and expense ratio.

Investing without a goal — Know what you are investing for. A clear goal helps you choose the right fund type and stay motivated during volatile periods.

Ignoring the expense ratio — The expense ratio is the annual fee charged by the fund. Over decades, even a small difference in expense ratio can significantly impact your final returns. Prefer low-cost index funds.

Final Thoughts

SIP is not a get-rich-quick scheme. It is a get-rich-steadily system that works remarkably well over time. The discipline of investing a fixed amount every month, the mathematical advantage of rupee-cost averaging, and the exponential power of compounding all combine to make SIP one of the most reliable paths to long-term wealth.

Start with whatever amount you can. Increase it as your income grows. Stay invested through market cycles. And let time do the heavy lifting.