Funding a university education is one of the most significant financial decisions a young person and their family will face. Tuition fees, accommodation, books, and living expenses can add up to a very substantial sum — and for many students, taking on some form of debt is unavoidable.

The two most common borrowing options for education are a student loan and a personal loan. While both give you access to money you need, they are fundamentally different products with very different terms, costs, and consequences.

This article explains both options clearly so you can make the best decision for your situation.

What Is a Student Loan?

A student loan is a type of loan specifically designed to help students pay for higher education expenses. These loans are typically offered by governments, banks, or dedicated education finance institutions.

Key characteristics of student loans:

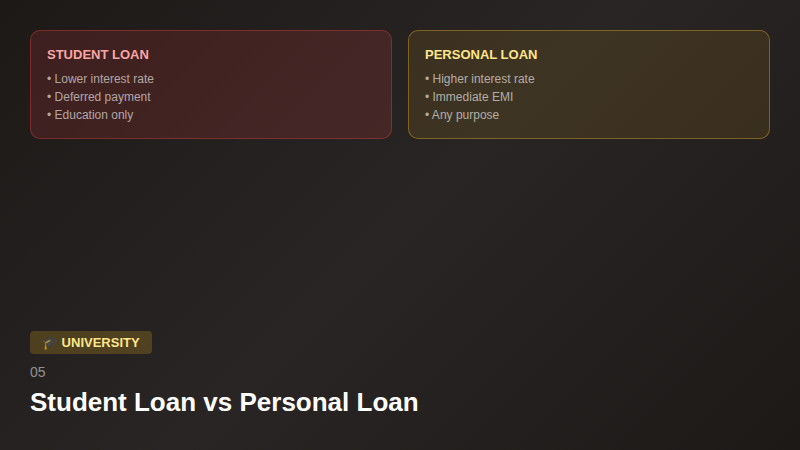

- Specifically designed for education costs — tuition, accommodation, books, living expenses

- Often come with lower interest rates than standard loans

- Many government-backed student loans offer subsidized interest (meaning the government pays the interest while you are still studying)

- Repayment usually begins only after you graduate and start earning above a threshold income

- Longer repayment periods — sometimes 10–25 years

- Some programs offer income-based repayment where monthly payments are tied to what you earn

- In some countries, certain student loans can be forgiven after a set period under specific conditions

What Is a Personal Loan?

A personal loan is a general-purpose loan offered by banks and financial institutions that can be used for almost anything — home renovation, medical emergencies, travel, or education.

Key characteristics of personal loans:

- Not specifically tied to education — can be used for any purpose

- Interest rates are typically higher than student loans

- Repayment begins immediately after the loan is disbursed, regardless of your employment status

- Shorter repayment periods — usually 1–7 years

- No government subsidies or income-linked repayment options

- Approval depends heavily on credit score and income (which can be a problem for students with no income)

Key Differences at a Glance

| Feature | Student Loan | Personal Loan |

|---|---|---|

| Purpose | Specifically for education | Any purpose |

| Interest rate | Lower (often subsidized) | Higher |

| Repayment start | After graduation or income threshold | Immediately |

| Repayment period | Long (10–25 years) | Short (1–7 years) |

| Collateral required | Usually not (especially govt loans) | Sometimes |

| Income required to apply | Not always | Often yes |

| Special benefits | Subsidies, tax benefits, possible forgiveness | None |

Interest Rate Deep Dive

The interest rate difference between student loans and personal loans is one of the most important factors to consider, because it determines the total amount you repay over the life of the loan.

Student loans — particularly government-backed ones — often carry interest rates significantly below what you would pay on a personal loan. Over a repayment period of several years, even a difference of a few percentage points in interest rate can translate into thousands of additional dollars paid on a personal loan.

Additionally, many student loans are subsidized — meaning the government pays the interest on your behalf while you are enrolled in university. With a personal loan, interest begins accumulating from day one.

Repayment Flexibility: A Critical Factor for Students

One of the biggest advantages of student loans for university students is repayment flexibility.

With most student loans, you do not have to make any repayments while you are studying. Repayment typically begins only after you graduate and start earning. Some income-linked repayment plans mean your monthly payments are calculated as a percentage of your salary — so if you earn less, you pay less.

Personal loans, on the other hand, require monthly repayments starting almost immediately. For a student with little or no income, this creates immediate financial pressure and can lead to missed payments, which damages your credit score.

When Might a Personal Loan Make Sense for Education?

Despite the general advantages of student loans, there are specific situations where a personal loan might be considered:

- You do not qualify for a student loan — due to income limits, citizenship requirements, or course type restrictions

- The institution is not eligible — some student loan programs only cover accredited institutions; for short courses or bootcamps, you may need a personal loan

- You need money faster — personal loan approvals can sometimes be quicker

- You need flexibility on how the money is used — student loans sometimes restrict what you can spend funds on

Even in these cases, compare interest rates carefully and explore all student loan options first.

Tips for Borrowing Wisely for Education

Borrow only what you need. It can be tempting to borrow a larger amount “just in case,” but every extra unit of currency borrowed is money you will repay with interest.

Understand the total repayment amount. Before signing any loan agreement, calculate the total amount you will repay over the full loan period — principal plus all interest. This is the true cost of your education borrowing.

Read the terms carefully. Look for fees, prepayment penalties, conditions for deferment, and what happens if you miss a payment.

Explore scholarships and grants first. Before taking on any debt, exhaust all free money options — merit scholarships, need-based grants, university bursaries, and government education grants. These do not need to be repaid and should always be pursued first.

Start repaying early if you can. Even while studying, if you have part-time income, making even small voluntary repayments toward your loan reduces the principal and saves significant interest over time.

Final Verdict

For the vast majority of university students, student loans are the better option for funding higher education. They offer lower interest rates, flexible repayment tied to your income, government subsidies, and longer repayment periods.

Personal loans have their place — for specific situations where student loans are not available or sufficient — but the cost and repayment pressure make them a less suitable primary option for most students.

Always research the student loan options available in your country first, apply early, and borrow only what you genuinely need.